eCommerce Isn't Taking Share. It's Taking Control.

Channel Intelligence Report

The penetration rate debate is a distraction. The real battle is over who owns the workflow and its already being decided.

Home Depot didn’t spend $23 billion on SRS and GMS to capture eCommerce transactions. QXO didn’t spend $13 billion on Beacon and Kodiak to sell shingles online. They spent it to own the system contractors use to run their business.

A contractor opens an app. Checks order history. Reorders the same SKU to a new jobsite. Closes the app. Your product was either in that order — or it wasn’t. Either way, you probably don’t know.

These aren’t price checks. These aren’t one-off special orders. This is workflow.

Whoever owns the workflow owns what comes next — the repeat purchase, the adjacent buy, the knock-on order your rep never knew was up for grabs.

New research from Zonda confirms it: eCommerce in building products isn’t a channel shift. It’s a control shift. Here’s what the data shows and what it means for every manufacturer watching from the sideline.

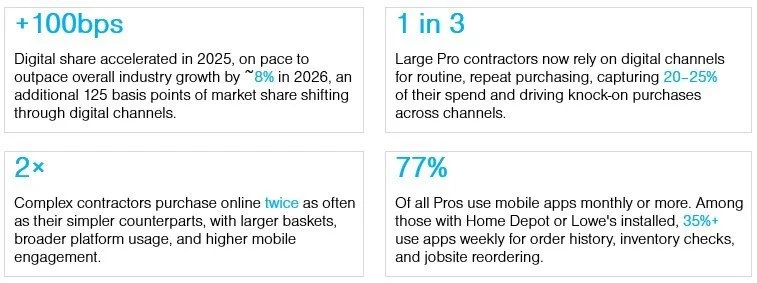

The Data That Proves It

The Zonda research doesn’t just show eCommerce growing. It shows where it’s growing. That distinction is everything.

Look at what those numbers are actually describing. It isn’t a spike in online orders. It’s contractors building digital systems into how they manage jobsites. Order history. Inventory checks. Reorders triggered by project milestones, not browsing decisions.

That’s why 77% of Pros are in mobile apps monthly. Not because the apps are convenient. Because the apps are now how the work gets organized.

Organized systems don’t get replaced easily.

“The digital relationship, not just the transaction, is increasingly determining supplier influence over knock-on purchases.” - Zonda Research, 2026

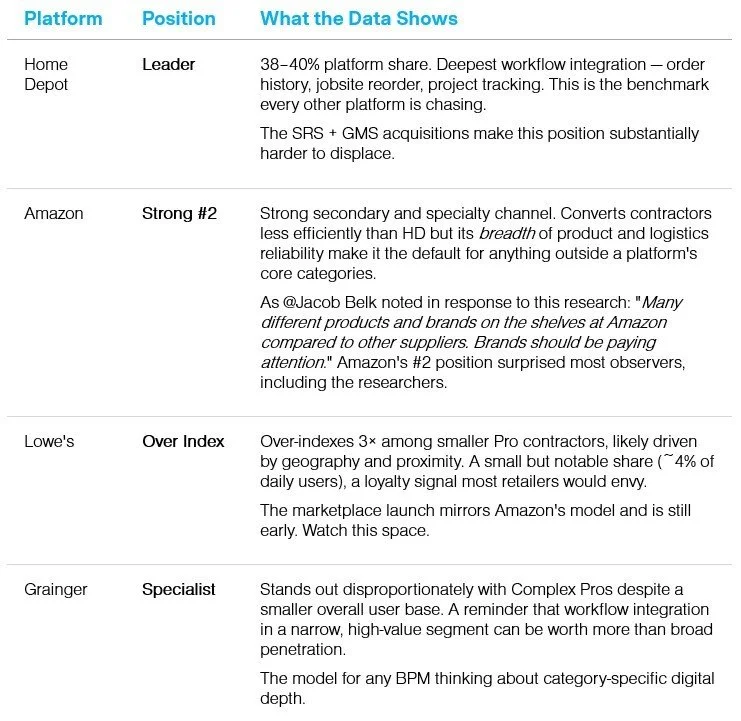

Who’s Winning the Workflow — and One Surprise

Not all platforms are winning the workflow battle equally. The Zonda data maps out a clear hierarchy, and one finding that should make every manufacturer rethink their channel assumptions.

If your brand doesn’t have a deliberate Amazon strategy, you don’t have a complete channel strategy.

The Timing Problem: Why This Matters More Right Now

Zonda’s principal Todd Tomalak added a critical observation to this research: “during periods of price volatility and shifting elasticities, market share tends to shift faster”. We saw it during COVID. We saw it during the Global Financial Crisis. And we are in one of those periods right now.

In an earlier issue of Building Blocks, we covered how tariffs and mega-distributor consolidation are compressing margins from both sides simultaneously, what I called the the Cost-Price Vise. Steel tariffs up 40%. QXO and HD now controlling 35%+ of pro distribution. Pricing power shifting to the channel.

The same conditions that are squeezing your margins are also accelerating the digital share shift.

When contractors are watching every dollar, they lean harder into the platforms that give them price visibility, order history, and fast fulfillment. That behavior becomes habit. And habits are hard to unwind when the market recovers.

Tomalak also noted that renovation demand is more favorable than new construction right now. With 60%+ of U.S. homes over 40 years old and tappable equity still substantial, the renovation super-cycle is loading. When it releases, the market share positions established during this slower period will determine who captures the surge.

The workflow relationships being built today are the distribution agreements of tomorrow.

THE COMPOUNDING PROBLEM:: In a down market, the instinct is to protect cash and wait. But waiting during a period of workflow digitization is not neutral. Every week a contractor embeds a competitor’s platform into their daily routine, your re-entry cost increases. The cost of delay is not deferred — it compounds quietly in the background.Different Starting Points. Same Endgame.

The M&A happening in parallel with this workflow data shift is not a coincidence. It’s the same strategic logic playing out at different scales.

Home Depot acquired SRS Distribution ($18B) and then GMS ($5.5B) with an explicit strategy of serving contractors “across their entire project” and increasing share of wallet. QXO assembled Beacon ($11B) and Kodiak ($2.25B) to build a scaled, technology-forward distribution platform. These are not bet-the-company acquisitions made for short-term revenue. They are infrastructure plays built to own more of the system through which contractor purchasing flows.

In Something Big Just Shifted, I wrote that the building products channel changed more in 90 days than in the prior nine years. The Zonda data is the behavioral evidence underneath that structural observation.

The M&A was the architecture being built. The workflow digitization is the behavior adapting to that architecture. Both are now compounding in the same direction.

THE UNCOMFORTABLE IMPLICATION FOR MANUFACTURERS: retailers and platforms are not optimizing for the sale. They are optimizing for the system the sale happens inside of. And systems scale differently. They don’t need to win every transaction. They just need to become the default.Once a platform is the default, the dynamic inverts. The contractor isn’t choosing between your product and a competitors at the point of sale. They’re reordering from the same place they ordered last time because their order history is there, their job codes are there, and switching platforms means rebuilding the administrative layer of how they run their business. That friction is your competitor’s moat. And it’s growing with every week a contractor uses the platform.

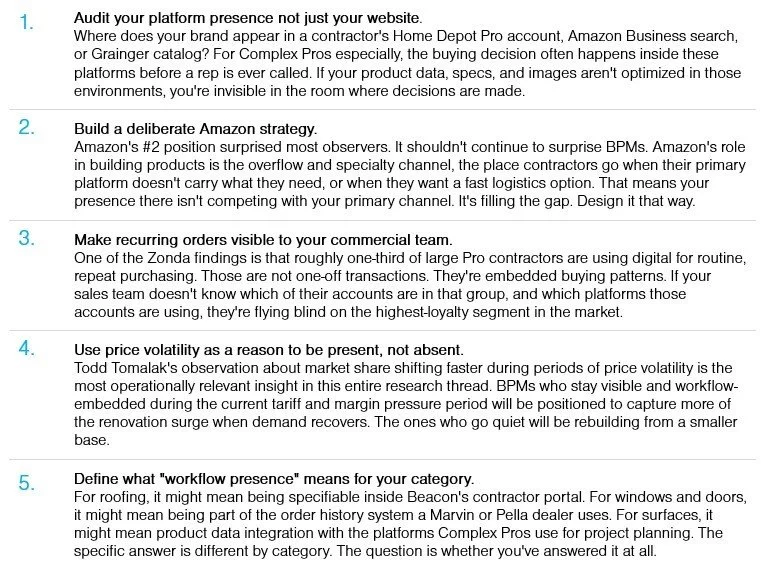

Five Moves. Pick One to Start This Quarter.

The question is no longer whether to engage with digital channels. It’s whether you’re engaging in a way that builds workflow presence or just transactional presence. They aren’t the same thing.

In the Channel-Proof eCommerce Framework I outlined in an earlier article, the core challenge was growing digital without burning your dealer relationships. That challenge is still real. But the Zonda data adds a new dimension: the platforms your dealers rely on are themselves becoming workflow infrastructure for the contractors you both serve. The question isn’t just “can I grow online without upsetting my dealers?” It’s “am I building any presence in the systems where my buyers are now making decisions?”

Two Positions. One Is Getting Harder to Recover From.

This isn’t really an eCommerce story. eCommerce is just the delivery mechanism for a deeper shift in where purchasing control lives.

The penetration rate —20%, 25%, wherever it settles — is the visible part of this change. The invisible part is the workflow layer being built underneath it. That workflow layer is what determines supplier influence, purchasing loyalty, and who gets the knock-on order. And the companies currently investing to own more of that workflow — through M&A, through platform development, through logistics infrastructure — are not doing it to capture eCommerce transactions. They’re doing it to determine what happens in the market around them.

The question is whether you have a strategy for being embedded in that workflow — or whether you’re planning to compete for business at the point of purchase in a system where someone else controls the interface.

Because those are two very different positions. The question isn’t whether this is happening. It’s whether you’re on the right side of it before the window closes.

EARLIER IN THIS SERIES

→ Something Big Just Shifted: Building Products Channel Is Being Rebuilt in Real Time

→ The Cost-Price Vise: How Tariffs & Consolidation Are Crunching Margins

→ Your Dealer Is Not Your Frenemy: A Framework for Channel-Proof eCommerce

Data attribution: Market data drawn from Zonda’s 2026 pro contractor eCommerce research, as presented by Todd Tomalak, Principal at Zonda. Additional context from Zonda’s Building Products Outlook and publicly available Mamp;A reporting on QXO, Home Depot, SRS Distribution, GMS, and Beacon Roofing Supply. Commentary from Jacob Belk and Todd Tomalak on the original research post informed the Amazon and price-volatility sections of this article.

If you’re a CEO or revenue leader in building products, AEC or consumer durables and want practical growth systems — subscribe. I publish weekly.

If you’re ready to diagnose what’s happening inside your own revenue system, Let’s talk.

Denine Harper | Fractional CMO | DHx Consulting

Explore my services →